Wipro Ltd. v. DCIT

Facts of the case:

This case law is the Karnataka High Court judgment pronounced on 25th March, 2015, which covers elaborately many domestic and international tax issues. In our discussion, we shall be limiting the analysis toasignificant international tax matter covered by this case law.

The following is the significant international tax issue pertaining to this case law discussed in this article:

- The assessee has claimed tax credit on Foreign Taxes paid on export income from USA and Canada which is exempt u/sc. 10A of the Income – tax Act, 1961 (‘the Act’). The assessing officer has disallowed claim of such credit as such income is exempt in India by virtue of Sec. 10A of the Act and there is no double taxation for providing double taxation relief through the credit mechanism

The Revenue’s Contention:

The assessee’s claim of foreign tax credit is on the ground that the entire earnings in respect of claim under Sec. 10A have been included in computing the total income. Sec. 10A which is appearing under Chapter – III refers to “incomes which do not form part of total income”. It is, therefore, clear in the first instance income falling u/sc. 10A did not form part of total income of the assessee in India. Since Sec. 10A falls under Chapter III, it does not therefore partake of the nature of total income chargeable to tax as per the provisions of Sec. 4 of the Act. In the second instance, no tax was paid on this income. The credit is being claimed under the provisions of Sec. 90, which is applicable for the grant of relief in respect of income on which have been paid both income tax under this Act and Income tax in the foreign country. The issue of credit u/sc. 90 clearly does not arise.

Assessee’s Contention:

Sec. 90(1) (a) (i) provides, if the income is subjected to tax, both in India and in the foreign country, the foreign income taxes paid attributable to such income are allowed as credit in India. However, Sec. 90(1) (a)(ii) is in respect of DTAA for granting of relief in respect of income tax chargeable under the Act and under the corresponding law in force in that country to promote mutual economic relations, trade and investment. Sec. 10A income is chargeable to tax in view of Sec.4 of the Act and is includible in the total income under section 5, but no tax is charged on such income because of the exemption given under section 10A,subject to the assessee satisfying the conditions prescribed. Once the assessee is made to pay tax on such exempted income in the other contracting State then Sec. 90(1)(a)(ii) enables him to claim credit of the tax paid in the contracting country.

The Hon’ ble High Court’s view:

Present Sec. 90 came into force from 01.04.2004. Extract of memorandum explaining provisions in the Finance Bill 2003 relevant to Sec. 90 read as follows:

“Under the existing Sec. 90, the Central Government may enter into an agreement with the Government of any country outside India for granting of relief in respect of income on which have been paid both income – tax under the Income – tax Act and income – tax in that country, or for the avoidance of double taxation of income under this Act and under the corresponding law in force in that country, etc.

In order to encourage international trade and commerce, it is proposed to insert a new clause in sub – section (1) of Sec. 90 so as to provide that the Central Government may also enter into an agreement with the Government of any country outside India, for granting relief in respect of income – tax chargeable under this Act or under the corresponding law in that country to promote mutual economic relations, trade and investment.”

With effect from 01.04.2004, Clause (a) (ii) of Sec. 90 (1)was substituted to provide for entering into an agreement for granting relief in respect of income tax chargeable under this Act and under corresponding law in force in that country, to promote mutual economic relations, trade and investment. Prior to the amendment, the relief was granted in respect of income on which income tax is paid under the Income tax Act and in the contracting country. Therefore, to get the benefit of the said provision, payment of income tax in both countries was sine qua non. However, by the amendment made by the Finance Act, 2003, the benefit of granting the relief was extended to even income tax chargeable under the Act and under the corresponding law in force in the other country. Therefore, the payment of income tax in both jurisdictions is not sine qua non anymore for granting the relief.

In cases covered u/sc. 90(1)(a)(ii) of the Act, it is not a case of the income being subjected to tax or the assessee has paid tax on the income. This applied to a case where the income of the assessee is chargeable under this Act as well as in the corresponding law in force in the other country. Though income tax is chargeable under the Act, it is open to the Parliament to grant exemptions under the Act from payment of tax for any specified period. Normally it is done as an incentive to the assessee to carry on manufacturing activities or in providing the services. Though the Central Government may extend the said benefit to the assessee in this country, by negotiations with the other countries, they could also be requested to extend the same benefit. If the contracting country agrees to extend the said benefit, then the assessee gets relief. In another scenario, though said income is exempt in this country, by virtue of the agreement, the amount of tax paid in the other country could be given credit to the assessee. Thus for the payment of income tax in the foreign jurisdiction, the assessee gets the benefit of its credit in this country.

Also Sec. 10A(1) provides that, subject to the provisions of the said section, profits and gains derived by an undertaking referred to in that section shall be allowed as deduction from the total income of the assessee. Therefore, by virtue of the aforesaid statutory provision, namely Sec. 10A of the Act, the income of the assessee from the exports in respect of the said unit is exempted from payment of income tax. The very fact that it is exempted from payment of tax means but for that exemption such income is chargeable to tax. By insertion of Clause (ii) in sub – section (1) (a) of Sec. 90, the Central Government has been vested with the power to enter into an agreement with the Government of any country outside India for the granting of relief in respect of income tax chargeable under the Income tax Act and under the corresponding law in force in that country, to promote mutual economic relations, trade and investment. Therefore, the statute by itself is not granting any relief. But, by virtue of the statute, if an agreement is entered into providing such relief, then the assessee would be entitled to such relief.

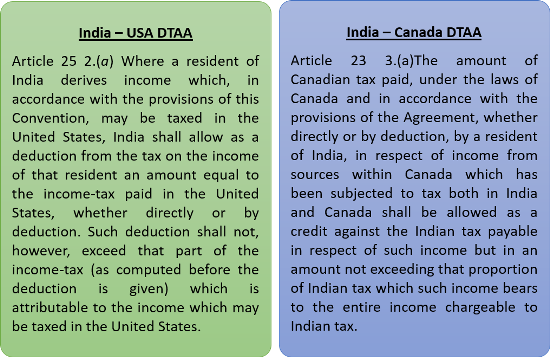

In case of India – USA DTAA, if a resident Indian derives income, which may be taxed in United States, India shall allow as a deduction from the tax on the income of the resident, amount equal to the income tax paid in United States of America, whether directly or by deduction. The conditions mandated in the treaty are that if any “income derived” and “tax paid in United States of America on such income”, then tax relief/credit shall be granted in India on such tax paid in United States of America. The said provision does not speak of any income tax being paid by the resident Indian under the Income – tax Act as a condition precedent for claiming the said benefit. Therefore, this provision is in conformity with Sec. 90(1) (a) (ii).

In case of India – Canada DTAA, the provisions make it clear that the benefit of Article – 23 would be available to an assessee in India only in respect of the income from sources within Canada, which has been subjected to tax both in India and Canada, which forms part of the total income of the assessee and has suffered tax in India under the Income – tax Act and has suffered tax in Canada also i.e., assessee has paid tax both in India as well as in Canada on the same income. Therefore, this provision is in conformity with Sec. 90(1)(a)(i).

Therefore, it is not the requirement of law that the assessee, before he claims credit under the India – USA convention or under the provisions of the Act, should pay tax in India on such income. However, in case of India – Canada convention if the assessee is exempted from payment of tax in India, then if the same is subjected to tax in Canada, according to the treaty there is no double taxation. Therefore, the benefit of the treaty is not available to the Indian assessee.

In so far as the issue related to credit of states taxes is concerned, section 91 provides relief from double taxation where no agreement under section 90 for the relief or avoidance of double taxation exists with a foreign country.

Explanation (iv) to Section 91 defines the expression “income-tax” in relation to any country to include any excess profits tax or business profits tax charged on the profits by the Government of any part of that country or a local authority in that country.

The intention of the Parliament is very clear. The Income tax in relation to any country includes income tax paid not only to the Federal Government of that Country, but also any income tax charged by any part of that country meaning a State or a local authority, and the assessee would be entitled to the relief of double taxation benefit with respect to the latter payment also.

Therefore, even though, India has not entered into any agreement with the State of a Country, the income tax paid in relation to that State is also eligible for tax credit.

Hence, the argument that in the absence of an agreement between India and the State, the benefit of Section 90 is not available to the assessee is ex-facie illegal and requires to be set aside.

Conclusion

This case law, among the other issues, has elaborately discussed the significance of Sec. 90(1)(a)(i) and Sec. 90(1)(a)(ii) of the Act. The case law provides clarity on situation where a foreign income suffering tax in the country of source and if the same is exempt in India, how should the credit on foreign taxes paid on such income be dealt with, whether the double taxation convention governing the said income is in consonance with Sec. 90(1)(a)(i) or Sec.90(1)(a)(ii) of the Act. Also in this decision of the high court, an elaborate discussion on chargeability of income to tax has been provided where the high court has taken the support of the Apex court decision in the case of Kasinka Trading and another v. Union of India and another in arriving at its conclusion that Sec. 10A income even though exempt is chargeable to tax for the purpose of Sec. 90(1) (a) (ii) of the Act.